- Ziggurat Realestatecorp

- Mar 17

- 3 min read

Britain’s faith in the housing market has always been strong. Before Christmas, we polled thousands of Britons about their money habits, and more people said they viewed property as a better place to invest their money over the next ten years than shares, savings accounts, or any other asset class. But in parts of the UK, that faith is being tested.

The average British home trebled in value between 1995 and 2005, but growth has been much more modest since. In fact, when adjusted for inflation — which, for some reason, people are loath to do when discussing house prices — prices are about a tenth lower now than at their pre-financial-crisis peak.

When we talk about the recent stagnation in Britain’s housing market, two segments usually attract the most attention.

The first is the decline at the very expensive end, mostly in London. Data from Zoopla on prices per square foot, based on valuations and sales, show just how steep those falls have been. In 2015, buyers in Chelsea were paying £1,704 per square foot, a price inflated by foreign investment and a thriving City. By 2025, prices had fallen to £1,227 — a drop of a quarter in nominal terms, or roughly half in real terms once inflation is factored in.

The second is the decline of the British flat. A quadruple whammy — the leasehold scandal, post-Grenfell safety concerns, declining investor appetite, and a general desire for more space — has pushed flat prices below their 2022 levels. By some estimates, nearly four in ten new-build leasehold flats in London are being sold at a loss. Other property types, meanwhile, have pulled away.

But how does this affect the housing ladder?

Buying a starter home in Britain is still expensive. A report by Deloitte puts the cost of a new-build flat in Britain at €5,203 per square metre (about £424 per sq ft), the third-highest among 25 European nations. In Italy, for example, the cost is roughly half that. Relatively high interest rates also mean first-time buyers are spending a substantial portion of their income on mortgage payments.

Yet after years of tight lending restrictions, banks are once again offering increasingly generous terms to new buyers.

Last week, Melton Building Society announced a 100 per cent loan-to-value mortgage. And, as a share of wages, first homes are not dramatically more expensive than the long-term average.

But what happens when those first-time buyers want to move on?

The traditional progression from starter home to stepping stone to dream home remains deeply embedded in the British property psyche.

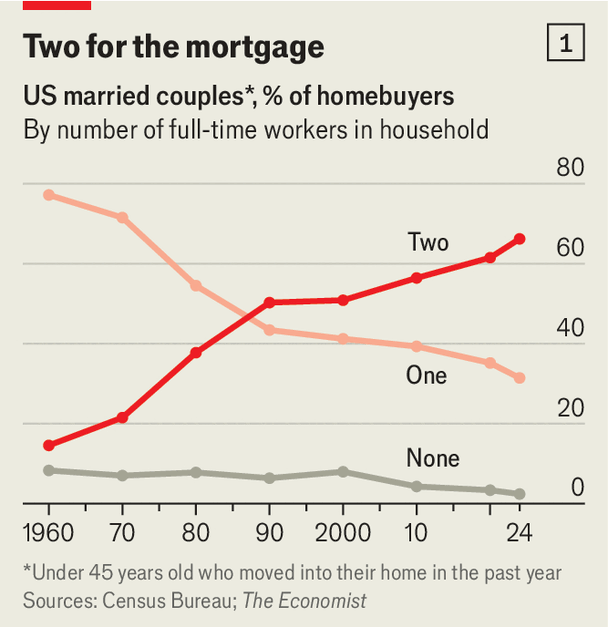

For baby boomers, climbing the property ladder was made easier by rapidly rising house prices. Imagine buying a flat in 1995 for £40,000 with a £10,000 deposit and selling it for £60,000 in 2000. Even excluding mortgage repayments, your £10,000 equity would have grown to £30,000. Yes, your dream home might have risen from £60,000 to £90,000 during that period — but you would now need only a 67 per cent mortgage to afford it.

Today, however, the first rung of the housing ladder offers far less lift. While today’s first-time buyers have an average household income of £61,000, those able to move a second, third, or fourth time typically earn around £93,000.

The cost of moving has also soared. Gordon Brown turned stamp duty into a major revenue-raiser in the 2000s, and George Osborne later increased it for high-value properties and introduced a second-home surcharge in 2016. The result is that moving home has become far less common. In the late 1990s, 7 per cent of homeowners moved each year; by 2024, that figure had fallen to just 3.9 per cent. Data from Savills suggest that while 35- to 44-year-olds made up 32 per cent of movers in the mid-2000s, that share has dropped to 24 per cent.

At the same time, under occupation — having more rooms than necessary — is increasing among older age groups, as would-be downsizers find it too expensive to move.

There has been a recent glimmer of hope that homeownership among young adults has begun to recover from its early-2010s lows. But increasingly, British homeowners are becoming stuck in the first homes they buy. The penny may have dropped that property is no longer a get-rich-quick scheme; more young people are turning to alternative investments to bridge the wealth gap instead of relying on house price growth.

Some first-time buyers are now going straight to their long-term homes, says Richard Donnell of Zoopla, sacrificing location and size in the process.

And so, as baby boomers in the southeast attempt to cash in on their multi-decade, seven-figure gains, they may find few buyers willing — or able — to trade up behind them.

Source: The Times