- Ziggurat Realestatecorp

- Apr 19

- 5 min read

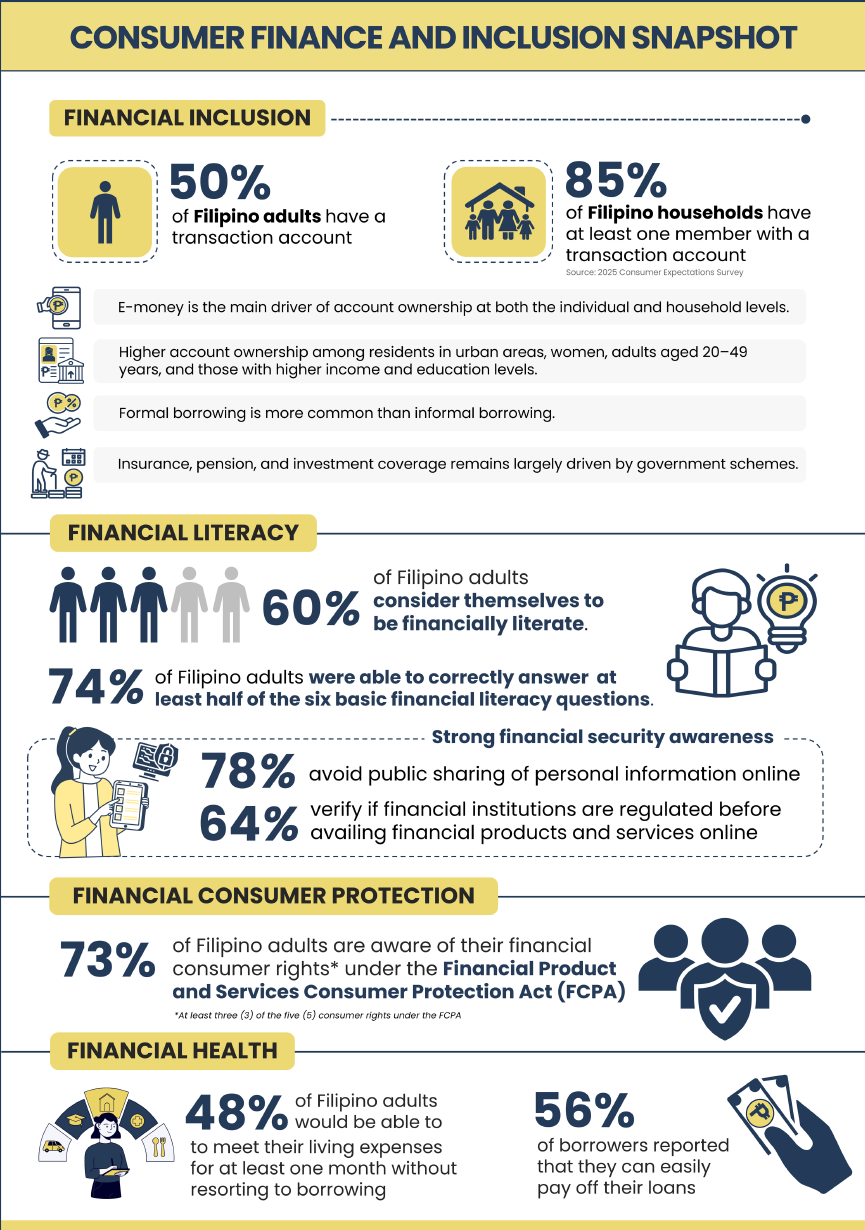

Half of Filipino adults had formal financial accounts in 2025, with gains recorded among the youth and women, a Bangko Sentral ng Pilipinas (BSP) survey showed.

According to the BSP’s 2025 Consumer Finance and Inclusion Survey (CFIS) released this week, 50% of Filipino adults owned bank, e-wallet, and other types of transaction accounts in 2025, down from 56% in 2021.

“This was partly driven by a decrease in transaction accounts linked to loans, particularly from microfinance institutions and cooperatives. This trend was consistent with the lower incidence of borrowing from these institutions,” the central bank said.

Adults with accounts with microfinance institutions and cooperatives went down to 5% and 2% last year, respectively, from 9% and 5% in 2021, the data showed.

“This decrease was aligned with lower loan incidence in these institutions: microfinance NGOs (nongovernment organizations) from 10% in 2021 to 6% in 2025, and cooperatives from 4% to 1% over the same period.”

Meanwhile, ownership of e-money and bank accounts remained steady at 36% and 23%, respectively.

At the household level, account ownership continued to grow, with 85% of households having at least one account in 2025, up from 74% in 2024, data from the BSP’s Consumer Expectations Survey (CES) showed. “While account ownership is uneven individually, household-level access is strong… This suggests that many families rely on shared financial access rather than individual account ownership.”

The BSP noted that women have surpassed men in ownership of more sophisticated accounts like bank accounts, which shows greater gender parity. Bank account ownership among Filipino women increased to 25% in 2025 from 20% in 2021, while men’s share stood at 22% last year versus 26% over the same period.

“Filipino women have consistently recorded higher account ownership than men since 2017, driven by the support of microfinance NGOs and in recent years, the expansion of e-money wallets and bank accounts,” it said.

“Beyond gender differences, disparities persist across income, education, and geography. Higher-income, better-educated adults are significantly more likely to own accounts. Regional differences remain pronounced, with urbanized regions showing higher ownership than predominantly rural areas.”

Account ownership among young adults aged 15 to 19 also rose to 34% in 2025 from 27% 2021, the central bank said, showing financial inclusion gains.

E-money was the main driver of account ownership at both the individual and household levels.

Digital finance also continues to grow as 62% of households said they used electronic devices for online financial transactions in 2025, rising from 53% in 2024, according to the CES.

This was driven by high levels of smartphone ownership, which rose to 86% in 2025 from 81% in 2021. The survey also showed that in 2025, 89% of Filipino adults said they use the internet, up from 77% in 2021, with over half (55%) doing so via mobile data.

“The BSP continues to work with government, private sector, and development partners under the National Strategy for Financial Inclusion 2022 to 2028 to broaden access to financial services. These efforts promote digitalization, financial literacy, consumer protection, and trust in the formal financial system, helping improve the financial health of all Filipinos.”

BORROWING, INVESTMENT

Meanwhile, the report also showed that formal borrowing is now more common than informal borrowing, showing progress toward “safer and more regulated” credit markets.

“While fewer Filipino adults are borrowing, at 25% in 2025 from 45% in 2021, the source of borrowing shifted from informal lending sources to safer and more regulated formal loans. In 2025, 16% of the total adult population borrow from formal channels such as banks, while only 10% relied on informal lenders. This marks a reversal from 2021, when informal borrowing was more common,” the BSP said.

Microfinance institutions remained the primary source of loans, but online lending platforms have also expanded their reach as more borrowers prioritize fast loan processing and approval. Other important borrowing considerations are repayment period, interest rate, and ease of application.

“Personal loans are the most common, followed by salary loans, multipurpose loans, and business loans. Many continue to rely on borrowing to meet basic needs such as food, education, and health expenses,” the BSP said.

“Most borrowers demonstrated sound repayment behavior, with a majority paying on time or ahead of schedule. However, a sizable minority reported difficulty in repayment.”

Meanwhile, overall insurance coverage and pension participation among Filipino adults continues to be largely driven by government-led schemes. Voluntary insurance uptake remains limited, especially among lower-income and less-educated groups, it said.

The data also showed that only 23% of adults reported having an investment in 2025, down from 36% in 2021.

“Overall investment participation declined compared with earlier years, and voluntary investment activity remains low, reflecting constrained disposable income and limited risk appetite among many adults,” the central bank said. “Investment participation is concentrated among higher-income, better-educated, and older adults, with motivations centered on achieving life goals and preparing for emergencies.”

Progress was also seen in several aspects of financial health, but it noted that low income and less educated individuals remained vulnerable in terms of stability. “Challenges persist in emergency preparedness and in maintaining adequate liquidity to manage potential income shocks.”

LITERACY GAINS

Despite this, Filipinos’ financial literacy and capability have improved, the report showed.

In 2025, 74% of the surveyed adults were able to correctly answer at least half of the six financial literacy questions, improving from 69% in 2021. “Understanding of risk and diversification is relatively strong, while knowledge of interest rates — particularly compound interest — continues to lag,” the BSP said.

Meanwhile, 86% said they have a personal budget, but financial confidence remains limited, with only 43% of adults feeling satisfied with their current situation.

“This shows that financial control does not always translate into financial confidence or resilience. When given extra funds, households prioritize emergency savings and family support, reflecting strong social values but also highlighting limited capacity for formal saving and investment.”

Awareness of financial products and services is also high, with increased interest seen for virtual assets. “Filipinos also demonstrate strong financial security awareness. Around 78% avoid sharing personal information online, while 64% verify if financial institutions are regulated before transacting,” the BSP added.

Most are also aware of their consumer rights, it said.

The 2025 CFIS has 8,784 completed interviews of adult respondents aged 15 years old and above across all regions of the Philippines, The survey was conducted from Feb. 16 to July 24, 2025.

“The 2025 CFIS highlights that financial inclusion in the Philippines has achieved broad reach, particularly through digital channels and household-level access. However, the findings also make clear that access alone is insufficient,” the BSP said.

“Sustained efforts are needed to deepen usage of financial products and services beyond transaction accounts, improve financial capability, and enhance consumer protection.”

Source: Business World