- Ziggurat Realestatecorp

- Apr 16

- 4 min read

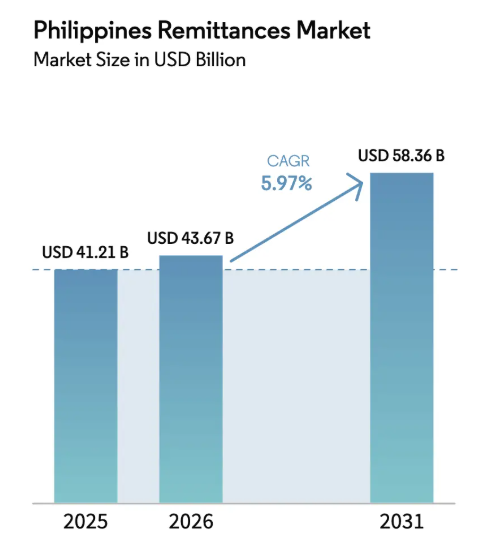

Overseas Filipino Workers (OFWs) remain one of the most powerful drivers of Philippine real estate demand. In 2026, that influence is being reshaped by new rules that regulate remittance fees, improve transparency in foreign‑exchange conversion, and strengthen financial‑protection safeguards. For Filipino buyers and OFWs, this means lower hidden costs, clearer conversion rates, and a more predictable foundation for property‑buying decisions.

What’s changing in 2026

A proposed OFW remittance protection framework is moving toward final implementation in 2026, with core goals focused on:

Capping remittance fees charged by banks and money‑transfer operators, so a larger share of every dollar sent actually reaches the family in pesos.

Requiring clear disclosure of the Philippine peso equivalent before the transfer is completed, eliminating “phantom” FX losses.

Banning unauthorized deductions from OFW remittances before the funds land in the beneficiary’s account.

Introducing financial‑protection and literacy programs tailored for OFWs and their families, especially around managing abroad‑earned income at home.

The thrust of the policy is straightforward: treat remittances as a core pillar of household and national financial stability, not just a routine transaction.

How this affects OFW property‑buying power

For OFWs, every peso that stays in the transfer directly boosts their effective purchasing power in the Philippine property market.

Lower fees mean more net PHP per dollar:If a typical remittance loses less to fees and opaque FX spreads, the net amount received in pesos goes up. That can translate into larger down payments, shorter loan terms, or the ability to move up in price bracket or location.

Predictable peso amounts support better budgeting:When OFWs can see the exact peso value before sending, they can plan home loans, condo payments, and maintenance budgets with far more confidence.

Stable, foreign‑currency‑linked income matters in a peso market:Because OFW remittances usually come in stronger currencies (dollars, dirhams, ringgit, etc.), even small improvements in FX transparency sharpen their advantage in a peso‑denominated property market.

In practice, an OFW sending the same gross amount in 2026 may be able to stretch that money further than in previous years—especially if they choose the right channels and plan ahead.

Who benefits from the new rules

Several groups in the Philippine real‑estate chain stand to gain from more transparent OFW remittances.

OFW buyers and their families:Lower hidden costs and clearer FX terms make it easier to compare payment plans, developers, and locations without worrying about surprises after the conversion.

Banks and housing‑finance programs (e.g., Pag‑IBIG):More traceable, regular remittance flows can serve as stronger proof of income for mortgages and housing loans, potentially improving approval odds and supporting better terms.

Developers and REITs targeting OFWs:With remittances growing in both volume and transparency, OFW‑linked demand becomes more predictable, which supports rental and occupancy assumptions for mid‑range condos, family homes, and provincial units.

The new rules essentially strengthen the plumbing of the entire OFW‑linked property ecosystem, making remittances a more reliable engine of demand.

How OFWs and families can maximize buying power

To turn these new rules into real‑estate advantage, OFWs and their families should focus on practical, disciplined steps.

1. Track net remittance amounts

Keep a simple record of how much you send versus how much the family receives in pesos, including FX impact.

Use this “net‑in‑hand” figure as the base for your monthly budget, not the gross amount sent.

This discipline helps avoid over‑leveraging just because the originating currency feels strong abroad.

2. Choose regulated, transparent channels

Prefer banks, BSP‑supervised remittance providers, and reputable digital platforms that clearly post fees and FX rates.

Avoid “too‑good‑to‑be‑true” offers that hide large spreads in the exchange rate.

A slightly slower but fully disclosed transfer is usually more valuable to a property buyer than a flashy, opaque one.

3. Align remittances with loan and payment cycles

Structure home loans or installment plans so due dates match typical remittance cycles (e.g., monthly or twice‑monthly inflows).

This reduces the risk of missed payments, penalties, or emergency borrowing when cash flow becomes lumpy.

OFWs with stable monthly paychecks benefit the most from this kind of alignment.

4. Use remittances as documented income

Many housing‑finance and developer programs already accept remittance records as part of OFW income documentation.

With clearer, more transparent remittance trails, OFWs can:

Qualify for higher loan ceilings.

Push for longer tenures or more favorable terms.

Treat remittances not just as “support money” but as a formal, structured income stream for real‑estate planning.

How developers and investors should position in 2026

For developers and long‑term investors, OFW‑remittance reforms create a more predictable, rule‑based demand base.

Pricing and affordability:With OFWs losing less money to fees, they can absorb slightly higher prices—or demand better locations and amenities—without changing their gross remittance levels.

Marketing and branding:Messaging can shift from generic “buy from abroad” themes to positioning projects as compatible with protected, predictable remittances, which resonates with family‑oriented, risk‑averse OFWs.

Portfolio mix:OFW‑focused projects near metro corridors, BPO‑linked provinces, and tourism‑adjacent areas are more likely to benefit from stable remittance‑linked demand than purely speculative plays.

In 2026, the projects that stand out are those that build around remittance transparency, stable cash flow, and clear family‑centric benefits, not just speculative price appreciation.

Conservative vs aggressive OFW‑property strategies

Conservative OFW buyers (saving for family homes or small rentals):

Use regulated, low‑cost channels and treat remittances as a fixed, monthly income stream.

Focus on stable, cash‑flowing units near family, schools, or work hubs rather than highly leveraged, high‑end bets.

Aggressive OFW‑investors (targeting rental portfolios or land banking):

Channel remittance savings into a structured property ladder: start with a smaller, manageable unit, then scale up using equity and refinancing once the portfolio is seasoned.

Consider diversifying into REITs or fractional‑ownership schemes if direct ownership feels too complex or risky.

Both approaches can coexist in a single portfolio: a core of stable, family‑oriented properties supported by a smaller, higher‑risk, higher‑growth slice.

Turning remittance rules into real estate advantage

The OFW remittance rules shaping up in 2026 are not just about consumer protection—they’re also about making remittances a more powerful, predictable engine of Philippine property demand. For Filipino families and OFWs, the key is to treat remittances as a serious, formalized income stream: track net flows, choose transparent channels, and align timing with mortgages and payment plans.

For developers and investors, the message is clear: projects that design around remittance transparency, stable OFW‑linked income, and family‑centric value will have a stronger edge in 2026 than those still relying on loose, undocumented expectations.

Source: Ziggurat Real Estate