Finding Bargains in Commercial Real Estate

- Ziggurat Realestatecorp

- Jul 11, 2023

- 9 min read

A steep slide has put a variety of real estate investment trusts on sale, from offices to datacenters. How to invest for growth and dividend yields around 6%.

Paul McDowell’s business has seen happier days. He runs Orion Office REIT, a real estate company that owns 81 office properties with an 88% occupancy rate. But hybrid work has hurt profits and demand for new offices. Since going public in late 2021, Orion’s stock is down 74%.

“Being in the office sector is not necessarily the easiest place to be,” Orion’s (ticker: ONL) McDowell told a recent investing conference in New York, looking at his sparse audience.

The great debate in real estate is whether the vacant office buildings in many cities will ever refill. Office vacancy has reached nearly 25% in cities like San Francisco and Chicago. Office real estate stocks are down 50% from pre-Covid highs, while the REIT sector has lost 9.5% in the past year against the S&P 500’s 14.5% gain.

But offices are now just 3.4% of the $1 trillion public market for real estate investment trusts, or REITs. The broader REIT space isn’t as troubled. With valuations laid low, there are bargains amid the rubble.

Some sectors are thriving, including warehouse/logistics properties and data centers. Apartment owners are enjoying healthy rental demand, as home buyers stay sidelined by 6.5% mortgages with average monthly payments that have doubled to almost $3,000 since early 2022, according to Apollo Group chief economist Torsten Sløk.

Even the office space offers opportunities. Some Sunbelt and suburban areas are seeing healthy occupancy and rents. Office REITs, while troubled, are now deeply discounted. Hybrid work may be here to stay, but corporations are pushing workers to return. Recent data show job postings for remote jobs have flattened.

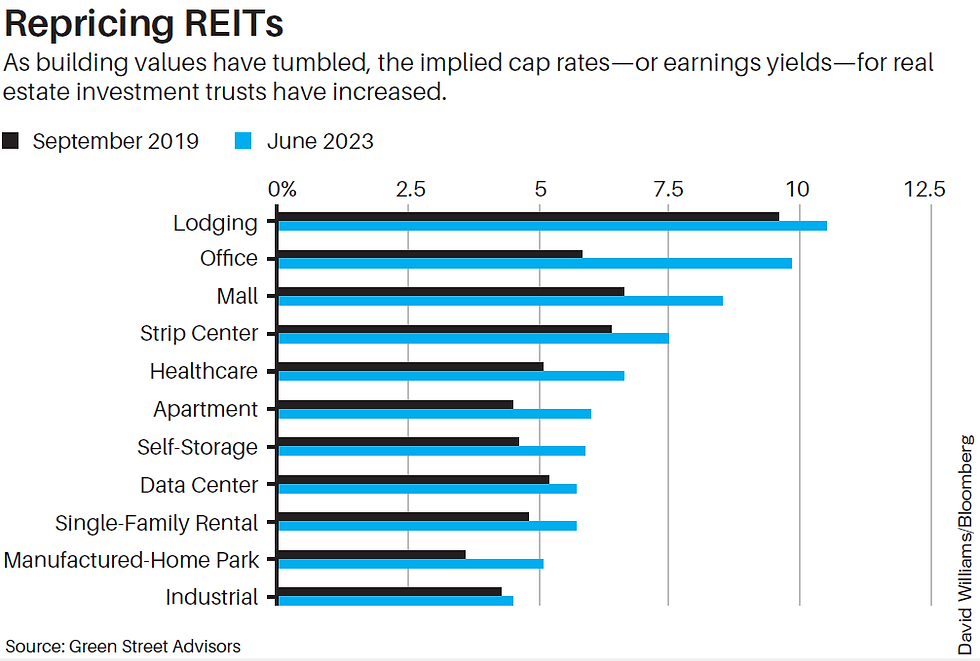

The selloff has delivered cheaper valuations and higher dividend yields. REITs, which must pay out almost all taxable profits as dividends, are yielding an average 4.1%, roughly double that of the S&P 500. After a large correction, REITs also look cheaper on measures of value such as the capitalization rate, or “cap rate”—which is like an earnings yield on rental properties. Cap rates now average nearly 7%, up from 5.5% before the pandemic, according to real estate analytics firm Green Street Advisors.

The sale prices reflect the fact that conditions aren’t yet favorable. A recession may lie ahead. The Federal Reserve hasn’t signaled that it’s done raising rates. And few of the bankers who make real estate loans are taking calls, frozen by higher rates, tighter lending standards, and loan-loss provisions— worries that the Fed highlighted in a recent report on financial stability.

“The most striking thing right now is the delta between fundamentals on the ground, which are pretty good, and lending conditions, which are pretty tight,” says Cedrik Lachance, research chief at Green Street Advisors. “Lenders don’t want to play ball right now.

” Yet real estate stocks are quite sensitive to economic data, reviving when leading indicators turn up. And compared with privately held real estate, which hasn’t corrected as much, the public market looks cheap, according to economist Ed Pierzak of the National Association of Real Estate Investment Trusts.

At the start of 2023, cap rates for public REITs were more than 15% above private real estate, Pierzak says. REIT total returns also fell nearly 40% behind returns for privately owned properties from 2022 to 2023— the biggest divergence in four decades. Gaps of that magnitude tend to close within a year, as cap rates and returns converge, he says, providing a potential tailwind for REIT stocks.

Debt also looks manageable for publicly traded REITs. It averages 34% of assets, down from 65% during the 2008-09 financial crisis. About three-quarters of that debt is unsecured bonds or bank loans, leaving REITs largely free of mortgage obligations. And almost 90% of REIT debt is fixed-rate, maturing in an average of seven years. That gives some breathing room. All told, REIT balance sheets can weather today’s tight credit environment.

One optimist is Willy Walker, CEO of commercial real estate financing firm Walker & Dunlop (WD). The company has been hit hard; Wall Street sees its earnings per share at around $4.90 this year, down from a peak of $8.15 in 2021. But after a lean 2023, the Mortgage Bankers Association trade group expects a revival in loan originations next year. Walker notes that his company hasn’t backed off its goal of increasing revenue 50%by 2025.

“The market is progressing at a slow pace,” he says. “But we remain focused on getting to those numbers.” One way to invest is with a barbell approach: Pair higher yielding stocks in hard-hit areas with those that aren’t as cheap but have strong growth trends and potential for capital gains. Here’s a look at some key REIT sectors and prospects within them.

Office

Some of the deepest values now are in office REITs, partly because leading indicators still look weak in many big cities. About 18% of office space was vacant at the end of the first quarter, up slightly from December’s vacancy rate, according to leasing firm CBRE. In Manhattan, with a 15.5% vacancy rate, the map is dotted with office towers that have fallen behind on payments or sold at a loss.

Why go bottom fishing? Because the stocks may now be fully discounted. Based on a real estate measure of cash flow called funds-fromoperations, or FFO, office REITs trade at nine times next year’s estimates. That’s just 55% of the S&P 500, using the analogous measure of earnings before interest, taxes, depreciation, and amortization.

“We just have to be patient and operate our way through it,” says Owen Thomas, CEO of BXP (BXP), the largest publicly traded office REIT, previously known as Boston Properties. While BXP’s stock has been hammered, down 15% this year after a 41% drop in 2022, its operating metrics aren’t bad. It has a 91% occupancy rate. The firm’s premier buildings in big cities still command top rents, and recent sales indicate those types of properties are in demand. Rival office REIT SL Green Realty (SLG) saw its stock pop nearly 20% after the company sold half its stake in a prime Park Avenue building in New York at a $2 billion valuation.

Investing now is a game of waiting for downtown office demand to rebound. Faster-growing Sunbelt markets are likely to recover a bit quicker, according to Lachance.

Two plays on that theme are Cousins Properties (CUZ) and Highwoods Properties (HIW). Cousins sports a 6% dividend yield and one of the lowest levels of debt in its sector. Recent leasing deals should return occupancy to pre-Covid levels, the company says. Highwoods also has low debt levels, with none due until the end of 2025. It has grown earnings for years by refreshing its portfolio to focus on Sunbelt cities.

“All REITs are being painted with the same brush,” complains Ted Klinck, CEO of Highwoods Properties. He notes that Highwoods has been tweaking its portfolio. It plans to buy buildings in Dallas, a fast-growing market, and sell in Pittsburgh, where prospects are less favorable.

Residential

Whereas Sunbelt REITs are preferred in the office market, they are temporarily out of favor in the residential market. A flood of new apartments under construction in many Southern markets could dampen rent growth for a year or two.

Analyst Steve Sakwa of Evercore ISI likes AvalonBay Communities (AVB) and Equity Residential (EQR), two REITs with big portfolios in coastal markets where apartment construction has been limited. Both companies are also considered good apartment operators and have moderate financial leverage, or debt levels.

Residential REIT stocks have fared better than office shares, so dividend yields remain around 3.5% at names like Avalon. That company’s roughly 300 properties are 96% occupied. Per-apartment rents and earnings are on track to rise 5% this year, according to Sakwa.

Equity Residential is the apartment network founded by recently deceased REIT pioneer Sam Zell. It also oversees about 300 properties, with 96% occupied and rents rising broadly. Equity enjoys a handsome 45% cash flow margin on its properties, yet its shares trade at an earnings multiple that’s below average for residential REITs.

One other play on residential real estate is single-family home rentals. Demand has been healthy, due to high mortgage rates and a drop in homes for sale. Jonathan Litt, founder of Land & Buildings, a real estate hedge fund, likes AMH (AMH), a REIT that owns nearly 59,000 single-family homes across 21 states. “People with kids can’t stay in an apartment and they can’t buy a home—so they rent,” Litt says.

AMH trades at a steep price/FFO of 21 and only yields 2.5%. But it has a dividend payout ratio of about 50% of FFO—implying plenty of dividend coverage and room to increase its payout. AMH carries low debt. It has also been a winning stock. It’s up 15% this year, beating the REIT average, which it has outperformed by an annualized eight percentage points over the past five years.

Retail

Retail REITs have been through the wringer as online shopping trends accelerated during the pandemic. Kimco Realty (KIM) operates strip centers, which are less affected by ecommerce than regional malls. Kimco’s niche is grocery-anchored shopping centers in stable inner-ring suburbs. CEO Conor Flynn tells Barron’s that remote work has helped, as homebound workers tend to shop more in suburban shopping centers. “They are going to local stores more than to the destination stores,” he says.

Earnings are dipping this year, reflecting higher interest expense, but should grow about 4% in 2024, according to consensus estimates. Kimco’s dividend yield is near 5% and looks covered with a 74% payout ratio of its adjusted FFO. Simon Property Group (SPG) is considered one of the best mall operators, with a 94.4% occupancy rate on March 31, up a percentage point from the year-earlier period. It also sports a balance sheet that’s stronger than most mall REITs, and yields 6.6% with enough cash flow to cover the payout.

The stock looks inexpensive at a price-to-FFO of about nine times, notes Green Street’s Lachance. The discount reflects anxieties about retail and consumer spending. But Lachance calls Simon a “best-in-class operator” with a low stock multiple that should price in “any kind of problems that will occur.”

Industrial

The rise of e-commerce has fueled huge gains for logistics and warehouse REITs. The country’s largest REIT now is Prologis (PLD), with a $140 billion enterprise value and plenty of cash for acquisitions—including a recent deal for 14 million square feet of properties purchased from Blackstone for $3 billion. Yet Prologis is also one of the priciest REITs on the market, with a relatively low 2.9% yield.

Less well-appreciated is First Industrial Realty Trust (FR). Its collection of distribution centers covers coastal markets, which are the best locations for such properties. First Industrial has wide margins, a betterthan- average balance sheet, and good management, according to Lachance. In presentations, the REIT notes that its properties are full and rents are rising. Yet compared with some other midsize industrial REITs, the stock trades at a bigger discount to operating earnings and book value, as investors overlook upgrades in its portfolio. The REIT’s yield is low, at 2.5%, but Wall Street sees profit momentum with FFO expected to rise about 6% this year and 9% in 2024.

Healthcare

Healthcare REITs own medical offices, nursing homes, and life-science research labs. Some of these stocks have floundered as investors worried about funding for biotech start-ups and the pandemic’s pause in office visits—though the latter trend has reversed, as patients come back for elective procedures.

One diversified healthcare REIT with a 6% yield is Healthpeak Properties (PEAK). It has a roughly even split of medical offices and life-sciences buildings. That provides both defensive stability and growth, says Lachance, who recommends the stock. Trading at about 11 times this year’s earnings—compared with a healthcare REIT average of 22 times—Healthpeak’s portfolio is one of the most-discounted in its sector, as investors worry about new supply of life-science space in key markets like Boston.

Yet the company faces few nearterm lease expirations in Boston. It has pulled back sharply on development, to conserve capital and capture better prices in a downturn. “When fundamentals turn, which they inevitably will, we expect to be in great shape to capitalize,” CEO Scott Brinker told investors in April.

Data Centers

A wave of private equity flooded into data centers over the past few years, aiming to profit off tech trends like cloud computing and corporate demand for connectivity. Data centers are on-ramps to the internet and the flywheels that keep it humming. Lease renewal rates are high, as the steep costs of switching to another site keep most tenants in place.

Mergers have consolidated data center REITs, leaving Equinix (EQIX) and Digital Realty Trust (DLR) in command of much of the market. Equinix stock has been a runaway winner, outperforming both Digital Realty and the S&P 500 for years. Digital is a contrarian value idea: It trades at a 50% discount to Equinix, based on FFO estimates, and it offers a 4.5% yield versus Equinix’s 1.8% payout.

The case for Digital is that it could be on the cusp of closing those gaps. The company has shored up its capital, by raising several billion from stock and property sales over the past few years. Cities around the world are now limiting new data-center builds. That restricts competition and gives incumbents like Digital more pricing power. “It’s not easy to build data centers anymore,” CEO Andy Power said at a recent conference.

Green Street’s Lachance admits that Digital stock has been a headache. But it goes for a 2023 FFO multiple of 16 times, compared with 35 times at Equinix. With an implied cap rate that is more than 1.3 percentage points higher than that of Equinix, Digital trades at a “monstrous” discount, he says.

Data REITs therefore present a classic barbell opportunity, with Equinix offering cloud-computing growth, and Digital Realty offering a higher yield on a discounted stock.

Source: Barron's

Comments